Nearly one in four American homeowners faces unexpected costs when tackling major home renovations. For Dallas-Fort Worth homeowners, relying on traditional insurance can leave you exposed to serious financial risks if things go wrong during construction. Understanding renovation insurance options can help you protect your investment, reduce stress, and avoid the shock of denied claims or surprise expenses as you upgrade your home.

Table of Contents

- Defining Renovation Insurance And Common Myths

- Types Of Renovation Insurance Policies Available

- What Homeowners And Contractors Need To Know

- Coverage, Exclusions, And Common Claims

- Costs, Process, And Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Renovation Insurance | Homeowners need specialized renovation insurance to cover risks excluded by standard homeowners policies, such as structural damages and contractor liabilities during improvement projects. |

| Types of Insurance Policies | Various policy types, including Builders Risk and Contractor Liability, should be considered to protect against specific risks in renovation work. |

| Insurance Responsibilities | Both homeowners and contractors must verify insurance coverage and understand exclusions to avoid financial vulnerabilities during renovation projects. |

| Financial Planning for Renovations | Accurate budgeting, including a contingency fund for unexpected costs, is crucial for successful home improvement, mitigating potential financial pitfalls. |

Defining Renovation Insurance and Common Myths

Renovation insurance represents a specialized protection mechanism designed to safeguard homeowners and contractors during property improvement projects. Unlike standard homeowners insurance, this unique coverage addresses the distinctive risks associated with renovation processes, including potential structural damages, liability concerns, and unexpected complications that can arise during construction.

Most homeowners mistakenly believe their existing homeowners policy will automatically cover renovation work. However, standard insurance policies typically exclude damages occurring during active renovation, leaving property owners financially vulnerable. This misconception can result in significant out-of-pocket expenses if accidents, property damage, or worker injuries happen during the project. Renovation insurance fills these critical coverage gaps by providing comprehensive protection specifically tailored to the dynamic and often unpredictable nature of home improvement work.

Understanding the nuanced risks is crucial. The EPA’s Renovation, Repair, and Painting Rule highlights how specialized renovation insurance becomes essential when managing potential hazards like lead exposure, structural modifications, and contractor-related liabilities. Common myths surrounding renovation insurance include believing it’s unnecessary, too expensive, or redundant with existing coverage. In reality, this targeted insurance can protect homeowners from substantial financial risks that standard policies explicitly exclude.

Pro tip: Before starting any renovation project, request a detailed review of your current insurance policy and specifically ask about renovation-related coverage gaps to ensure comprehensive protection.

Types of Renovation Insurance Policies Available

Renovation insurance encompasses several specialized policy types designed to protect homeowners and contractors during different stages of home improvement projects. HUD’s Section 203(k) program offers two primary insurance options: the Standard 203(k) for major renovations and the Limited 203(k) for less extensive repairs, providing comprehensive financial protection for both homeowners and lenders during renovation work.

Beyond mortgage-related insurance, homeowners can access multiple renovation insurance policy categories. Builders Risk Insurance covers property during construction, protecting against damages to materials, equipment, and the work-in-progress. Contractor Professional Liability Insurance shields renovation professionals from potential legal claims, addressing potential errors, design flaws, or negligence that might occur during project execution. This type of coverage is critical, as professional liability insurance helps mitigate financial risks associated with complex renovation work.

Additional renovation insurance policy types include Course of Construction Insurance, which provides comprehensive coverage for property damage during renovation, and General Liability Insurance that protects against third-party injury claims. Some specialized policies also cover unexpected structural discoveries, permit-related issues, and potential project delays. Homeowners should carefully evaluate their specific renovation scope and potential risks when selecting an appropriate insurance strategy.

Pro tip: Always request a detailed comparison of renovation insurance policies from multiple providers, ensuring you understand the exact coverage limits, exclusions, and specific protections for your unique renovation project.

Here’s a summary comparing major renovation insurance types and their primary protections:

| Policy Type | Primary Coverage Focus | Who Benefits | Typical Project Type |

|---|---|---|---|

| Builders Risk | Property during construction | Homeowner & contractor | New construction, major remodels |

| 203(k) Standard | Large renovation, full upgrade | Homeowner & lender | Major structural changes |

| 203(k) Limited | Smaller repairs, minor changes | Homeowner & lender | Cosmetic or minor fixes |

| Contractor Liability | Errors, negligence, legal claims | Contractor | Any renovation work |

| Course of Construction | Property damage during building | Homeowner | Extensive renovations |

| General Liability | Third-party injuries | Contractor & homeowner | All renovation projects |

What Homeowners and Contractors Need to Know

Both homeowners and contractors must thoroughly understand their insurance responsibilities during renovation projects. Homeowners insurance policies typically cover the home structure, personal belongings, and liability, but often contain critical limitations when it comes to renovation work. Liability coverage becomes particularly complex during construction, with potential gaps that could leave both parties financially exposed.

Contractors play a crucial role in managing renovation risks. They should carry their own comprehensive insurance that includes general liability, workers compensation, and professional liability coverage. Standard homeowners insurance may provide limited protection for worker injuries, making it essential for homeowners to verify a contractor’s insurance documentation before beginning any project. This verification process helps protect against potential lawsuits, property damage, and unexpected financial burdens.

Key insurance considerations for renovation projects include understanding specific policy exclusions, documenting existing property conditions before work begins, and maintaining clear communication between homeowners and contractors about insurance responsibilities. Renovation-specific insurance can bridge gaps in standard policies, covering unique risks like structural modifications, temporary property vulnerabilities, and potential project interruptions. Homeowners should request comprehensive insurance certificates from contractors and carefully review the scope of coverage to ensure complete protection throughout the renovation process.

Pro tip: Request a detailed insurance review from an independent insurance agent who specializes in renovation coverage to identify potential gaps and ensure comprehensive protection for your specific renovation project.

This table highlights key insurance documentation and verification steps to help homeowners and contractors minimize renovation risks:

| Step | Why It Matters | Who Does It | Potential Risk Reduced |

|---|---|---|---|

| Verify contractor insurance | Ensures valid coverage | Homeowner | Lawsuits, property loss |

| Document property condition | Establishes “before” status | Homeowner | Disputes, claim denial |

| Request insurance certificates | Proof of coverage | Both parties | Uninsured accidents |

| Review policy exclusions | Identify gaps in coverage | Both parties | Financial exposure |

| Maintain project records | Supports claim evidence | Homeowner | Claim rejection |

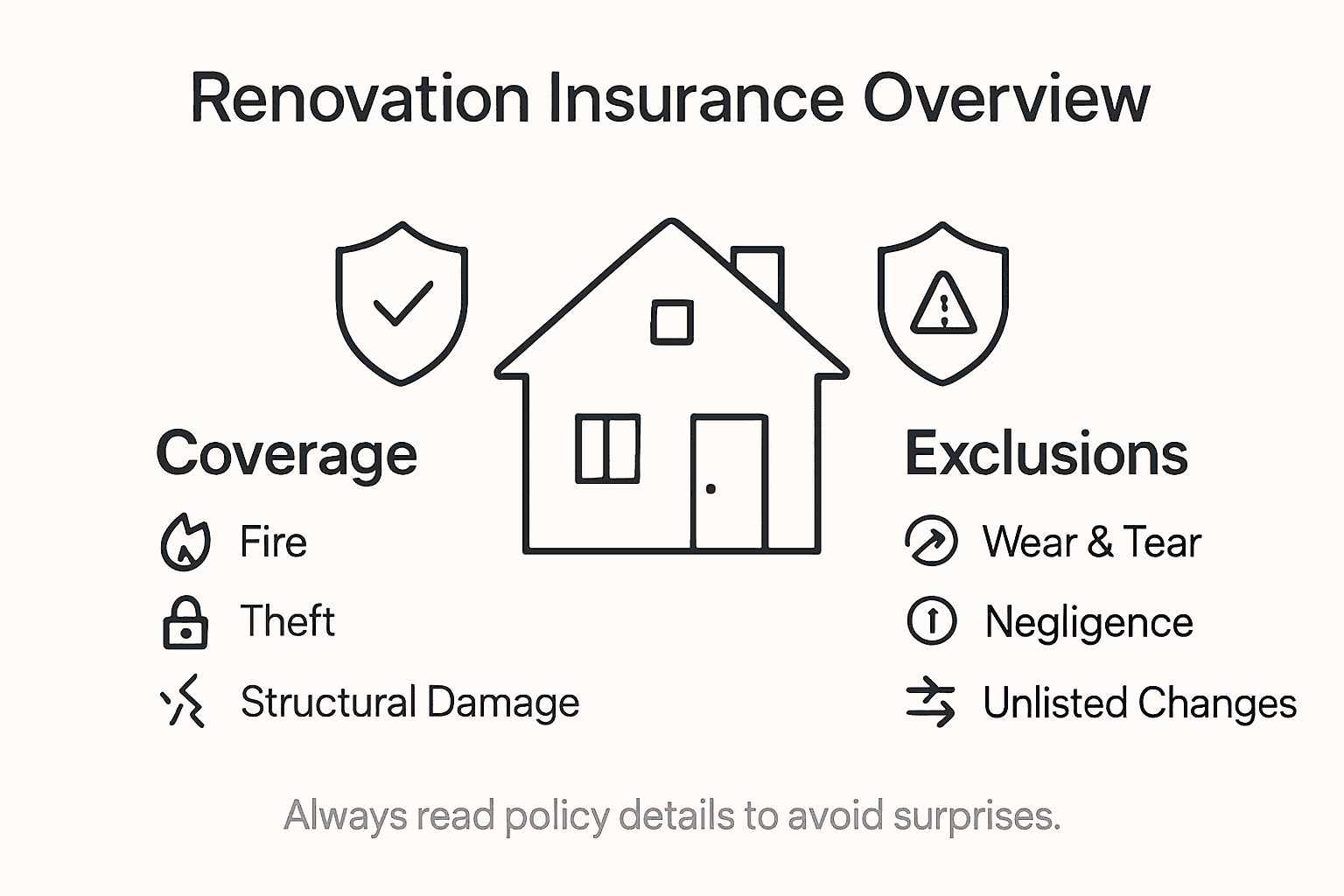

Coverage, Exclusions, and Common Claims

Understanding the nuanced landscape of renovation insurance requires a deep dive into policy exclusions and common insurance claims. Insurance providers strategically design policies to limit their risk exposure, which means certain high-risk construction activities and specific types of damage may be explicitly excluded from standard coverage. Residential construction defects, for instance, often fall into a gray area that can leave homeowners and contractors financially vulnerable.

Standard homeowners insurance typically covers damages from specific perils, including fires, storms, and theft. However, renovation projects introduce complex risks that may not be covered under traditional policies. Common exclusions include flood damage, earthquake-related losses, gradual wear and tear, and intentional property damage. Contractors and homeowners must carefully review policy language, paying special attention to endorsements that can provide additional protection for unique renovation-related risks.

The most frequent insurance claims during renovation projects typically involve structural damage, property loss, and liability issues. Accidental damage during construction, tool or material theft, and worker injuries represent significant potential claim scenarios. Homeowners should document existing property conditions before starting work, maintain detailed communication with contractors, and ensure comprehensive insurance documentation is in place. Specialized renovation insurance can bridge critical gaps in standard policies, offering protection for temporary property vulnerabilities, project interruptions, and specific construction-related risks.

Pro tip: Create a comprehensive digital file documenting all insurance policies, contractor certifications, and project specifications to streamline potential future insurance claims and protect your renovation investment.

Costs, Process, and Mistakes to Avoid

Home improvement financing requires meticulous planning and a comprehensive understanding of potential financial pitfalls. Construction cost estimation involves multiple complex components, including design expenses, material costs, labor, and unexpected contingencies. Homeowners frequently underestimate the total investment required, leading to financial strain and incomplete renovation projects. Accurate budgeting demands a systematic approach that anticipates potential challenges and builds in financial buffers.

The renovation process involves several critical financial considerations. Systematic cost estimation requires homeowners to account for capital costs beyond basic construction expenses. These include design fees, permit expenses, material procurement, labor, supervision, and potential financing charges. Common financial mistakes include failing to obtain multiple contractor estimates, neglecting to research material costs thoroughly, and overlooking potential hidden structural issues that could significantly increase project expenses.

Navigating the renovation financial landscape requires strategic planning and risk mitigation. Homeowners should develop a comprehensive budget that includes a 15-20% contingency fund for unexpected complications. Critical steps include verifying contractor credentials, understanding detailed project scopes, and documenting all financial agreements in writing. Specialized renovation financing options, such as home equity loans or renovation-specific lending programs, can provide more flexible funding strategies tailored to complex home improvement projects.

Pro tip: Create a detailed spreadsheet tracking every anticipated expense, including a dedicated column for unexpected costs, and update it weekly throughout your renovation project to maintain precise financial control.

Protect Your Renovation Investment with Expert Construction Services

Renovation insurance highlights the real risks that come with home improvement projects such as structural changes, liability gaps, and unexpected damages. Many homeowners face financial stress due to these uncovered risks. AstroTech Construction understands these challenges and offers professional remodeling and renovation services in the Dallas – Fort Worth Metroplex to help you avoid costly surprises. With expertise in full home remodeling, kitchen and bathroom upgrades, and storm damage repairs, we ensure your project is completed to the highest standards while minimizing insurance complications.

Ready to start your renovation with peace of mind? Visit AstroTech Construction to schedule a consultation and discover solutions tailored to your needs. Learn how our team’s quality assurance and unmatched service can protect your home improvement investment from common pitfalls discussed in What Is Renovation Insurance and Why It Matters. Don’t wait until risks turn into costly claims. Act now to secure expert guidance and construction that meets your expectations.

Frequently Asked Questions

What is renovation insurance?

Renovation insurance is a specialized type of coverage designed to protect homeowners and contractors during property improvement projects, safeguarding against risks such as structural damage, liability concerns, and unexpected complications that can arise during construction.

Why do I need renovation insurance?

Homeowners often mistakenly believe their standard homeowners insurance covers renovation projects. Renovation insurance fills critical coverage gaps, protecting against potential financial loss due to accidents, property damage, or worker injuries during the renovation process.

What types of renovation insurance policies are available?

There are several types of renovation insurance policies, including Builders Risk Insurance, 203(k) Standard and Limited policies, Contractor Professional Liability Insurance, Course of Construction Insurance, and General Liability Insurance, each tailored to address different risks and project types.

What exclusions should I be aware of in renovation insurance?

Common exclusions in renovation insurance typically include flood damage, earthquake-related losses, gradual wear and tear, and intentional property damage. It’s crucial to review policy language carefully to understand specific exclusions that may apply to your renovation project.

Recommended

- Why Renovate After Damage: Safety, Value, and Recovery – Astrotech Construction

- Complete Guide to Why Renovate Your Home – Astrotech Construction

- Renovation Permits Explained: Rules, Types, Costs – Astrotech Construction

- Complete Guide to Renovation vs Remodeling Differences – Astrotech Construction